This is a sequel to the popular articles: “COVID-19 Crash Course for Small Biz Payroll Protection Plan Applicants,” “A Quick, Easy Update on the CARES Act,” “CARES Act Potholes,” “The Big CARES Act Double Dip,” and “How to Borrow CARES Act Money and Legally Not Pay It Back”

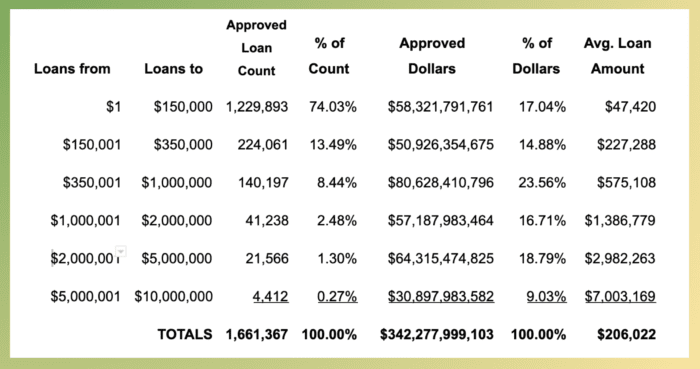

Nearly three-quarters of the loans went to the smallest of companies—those needing $150,000 or less. While slightly more than a quarter of a point of these loans went to the big players, those big borrowers took slightly more than 9% of the available funds.

EDITED BY GEORGE W. HIGHTOWER

The last Friday of the month is quickly transforming to CARE day for small businesses. On Friday, April 24, exactly four weeks after the CARES Act was signed into law on March 27, President Donald Trump signed into law the Paycheck Protection Program and Health Care Enhancement Act.

Once again, the Paycheck Protection Program (PPP) is the leading subject of this new legislation. But whereas the 880-page Coronavirus Aid, Relief, and Economic Security Act was designed with a spiffy pseudonym (CARES Act), the current legislation has no acronym and is only a few pages long.

Before I go any further, remember the number one rule I have noted in all of my CARES Act columns: only trust information from dot-gov websites.

Once you’re on the right site, you’ll see that the newest act replaces the “amount authorized for commitments for general business loans” by striking “$349,000,000,000” and inserting “$659,000,000,000.” For those who don’t like all those circles—$349 billion was just increased by $310 billion to $659 billion. Many news outlets are erroneously reporting the PPP adds $320 billion—that’s because Economic Injury Disaster Loans And Emergency Grants, known as EIDL loans (and pronounced “idle,” like a car at a stoplight) were increased from $10 billion to $20 billion.

Nevertheless, the maximum amount of a loan to a borrower remains at $10 million. Remember that figure. It gets important in a few paragraphs.

Little guys, heavy lifting

On Friday, April 17, US Treasury Secretary Steven T. Mnuchin announced that nearly 20% of the amount approved in phase one was processed by banks with less than $1 billion in assets, while approximately 60% of the loans were approved by lenders with $10 billion of assets or less. A billion sounds like a lot … until you get into banking or government, where billion-dollar banks are tiny. Consider that the size of the country’s 15 largest banks, according to bankrate.com, have assets from $2.74 trillion (JPMorgan Chase) down to lowly SunTrust, with assets of just $220.43 billion.

As a comparison, ibanknet.com lists 106 Massachusetts commercial banks. Aside from State Street (#13 nationally), 64 banks have less than $1 billion of assets, 38 have more than $1 billion but less than $10 billion, and only 3 have over $10 billion (topped by Berkshire Bank at $13.18 billion). Small businesses should consider supporting those banks that stepped up to the plate in the coronavirus chaos next time you’re looking for an institution to have a financial relationship with.

How far will this new money go?

Far, but likely not far enough, and it could be a bit more than $310 billion. Let’s look at the numbers. At noon on Thursday, April 16, just as the program was about to reach its funding limit, the Small Business Administration (SBA) released the program metrics (we added average loan amounts) included in the chart below.

Nearly three-quarters of the loans went to the smallest of companies—those needing $150,000 or less. While slightly more than a quarter of a point of these loans (think 27 pennies out of a hundred dollar bill) went to the big players, those big borrowers took slightly more than 9% of the available funds. Think of it this way: each average large borrower took the place of about 148 of the smallest borrowers.

The SBA had approved 1.66 million loans by the noon report above, and by the time the program was depleted, the count was likely closer to 1.7 million. If the program didn’t break 1.7 million loans, it now might, thanks to Danny Meyer.

Pigs get fat, hogs get slaughtered

It was widely reported that in the top tier of handouts, there were a number of large-dollar approvals to brand-name publicly-traded companies, including Shake Shack ($10 million), Ruth’s Chris Steak House ($20 million because chain steered around the $10 million cap by applying through two subsidiaries), Potbelly (another $20 million winner), and Fiesta Restaurant Group’s Taco Cabana chain ($10 million). The list keeps growing as reporters and researchers plow through Securities and Exchange Commission (SEC) filings and uncover the loan proceeds.

According to MarketWatch.com, “more than 100 public companies have received nearly $500 million in PPP funds,” relying in part on a Wall Street Journal report and Morgan Stanley research. These sorts of company announcements are filed with the SEC on Form 8-K. You can find them by visiting EDGAR, the SEC’s Electronic Data Gathering, Analysis and Retrieval system. Click the Shake Shack $10 million to view their 8-K filing.

The overly generous loans to publicly-traded companies sent shockwaves across social media, and pressure to return the money reached a boiling point quickly. Shake Shack founder Danny Meyer made headlines on Sunday, April 19 by wisely announcing on LinkedIn that Shake Shack would return its $10 million PPP loan and would instead raise capital in the public markets.

Nearly 96% of all the borrowers approved for PPP loans sought loans of $1 million or less. If the size distribution stays about the same, Meyer’s $10 million repayment could fund another 84 companies; 65 seeking the smallest loan band, 12 seeking the next highest, and 7 seeking loans up to $1 million. Senator Marco Rubio, chairman of the Senate’s Small Business Committee, tweeted that in addition to the $310 billion, there will be “an additional significant amount of money from #PPPloans being returned by several publicly traded large companies.” So one way or another, these repayments will help keep struggling small businesses open on main streets from coast to coast.

Out of the frying pan, into the fire

Not everyone had Danny Meyer’s foresight. Others have held firm, though there was a major change on Thursday, April 23, when the SBA issued another Paycheck Protection Program guidance update, adding question #31 to the list:

Do businesses owned by large companies with adequate sources of liquidity to support the business’s ongoing operations qualify for a PPP loan? You can read more here, but the essence, borrowers should first look at their ability to access other sources of liquidity sufficient to support their ongoing operations in a manner that is not significantly detrimental to the business. For example, it is unlikely that a public company with substantial market value and access to capital markets will be able to make the required certification in good faith, and such a company should be prepared to demonstrate to SBA, upon request, the basis for its certification.

The SBA then offered these larger players an out: “Any borrower that applied for a PPP loan prior to the issuance of this guidance and repays the loan in full by May 7, 2020 will be deemed by SBA to have made the required certification in good faith.” Following the update, Ruth’s Chris announced it was returning the $20 million. All things considered, it’s a reasonable expectation that as much as $100 million will be coming back quickly. That level of repayment can fund a boatload of smaller dollar borrowers.

Did the first round really run dry in the first few minutes?

Program pundits argue that the loans were consumed within the first few minutes of the spigot opening. A senior JPMorganChase executive stated that within the first five minutes of opening their program, the bank received over 60,000 applications. Yet when the SBA had exhausted its guarantees, only 27,000 Chase loans had been approved. Bank of America is rumored to have received over 10,000 applications per hour on opening day, but just “thousands” of those loans were ultimately approved by the SBA.

It isn’t clear how many applications the big banks actually submitted, and accusations and lawsuits are running rampant that the big banks like JPMorgan shuffled applications and favored larger corporate clients. CBS reports that JPMorgan provided these loans to four of the seven biggest known PPP borrowers. The SBA has stated that lenders should need no more than 30 minutes to review and process an application, since much of the loan approval is dependent upon the certifications supplied by borrowers. To understand why larger lenders might favor larger borrowers, let’s follow the money.

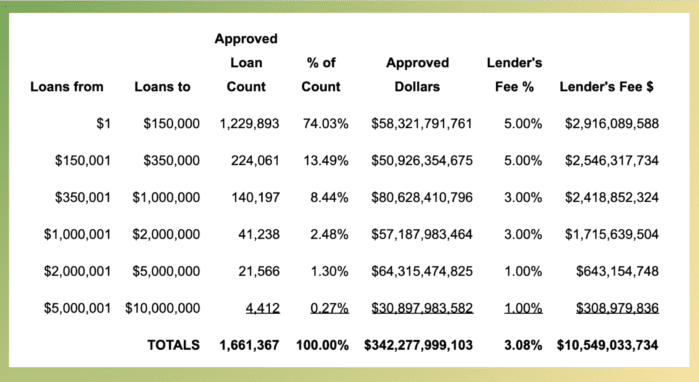

Lenders are paid fees by the SBA to process loan applications, document the transactions, and manage the loans. A lot of fees, $10.75 billion by our estimate to award and disperse the initial $349 billion. Loans up to $350,000 earn a lending fee of 5%. Loans to $2 million earn a lending fee of 3%. For loans above $2 million, the lending fee is 1% of the loan amount. And if the next round has fewer large borrowers, and in turn, far more smaller borrowers, that $310 billion could generate $10 billion or more of additional fees. The chart below shows that SBA data with the lender’s fee added on.

JPMorganChase arranged Shake Shack’s $10 million loan and so JPMC should have received a $100,000 fee for those services. To be fair, some of those fees are to offset the low 1% interest rate on the loans, but if the loan is to be forgiven, the bank is only out-of-pocket less than 7 months: 8 weeks for the loan; 60 days to review “an application for loan forgiveness under this section from an eligible recipient… [and] issue a decision on the an application”; and 90 days for the SBA to “remit to the lender an amount equal to the amount of forgiveness, plus any interest accrued through the date of payment.”

Checkout lines

Prospective borrowers generally applied through their favored bank. Once the application was reviewed and approved, the bank uploaded the application to the E-Tran system to secure an SBA guarantee. The E-Tran system is internet-enabled, so banks could have multiple people uploading applications. It was reported in the early days of the program that banks were expressing extreme frustration that they could not connect to E-Tran, not unexpected for a program that processed a normal year’s worth of SBA activity in a single day, for days on end.

Let’s compare this to a supermarket checkout line. All things being equal, you get out quickly by picking the shortest line. The next consideration is the size of each shopper’s order. Being second in line behind a family that is stocking up for a three-week quarantine might be slower than being number six in the express line, and so it went with the banks. Statistics are not readily available, but while the large banks may have a larger staff, they likely also had many more applications, such that each loan processor’s in-basket was overflowing with prospective borrower files.

The smaller community banks likely had a better app-to-loan-processor ratio, and therefore their lines may have moved faster. Thus, while thousands of prospective borrowers were stranded at the big banks, it seems the small banks ushered their customers through faster, much like the express line at the supermarket. For example, a friend applied to a local Rhode Island bank on opening day, Friday, April 3. On Tuesday, April 7, the bank requested some additional information and the completed package was submitted for an SBA guarantee two days later. He ultimately received approval for the full amount.

How fast will the $310 billion go?

Fast.

Many banks are reported to have applications that didn’t get uploaded to the SBA during round one. The SBA likely has a substantial amount of applications that didn’t get reviewed before funding ran out.

There is a specific $60 billion set aside for small-institution lenders. While anyone can apply there, these lenders are most likely servicing smaller, disadvantaged, or inner-city business enterprises. If you’re familiar with Massachusetts, download the list (link is below) and notice the markets these lenders serve (non-Bay Staters, don’t fret, the list is national).

It’s a way to help the really small businessperson. Some major news outlets are reporting the set aside is $30 billion, but they are likely referring to the smallest set aside (below). Don’t get confused.

The new act has set aside $30 billion for loans made by “insured depository institutions” and “credit unions with consolidated assets of not less than $10 [billion] and less than $50 [billion].” It might read awkward to the naked eye, but that means smaller lenders with assets between $10 billion and $49.999 billion.

There is another $30 billion set aside for loans made by “Community Financial Institutions, Small Insured Depository Institutions, and Credit Unions” with consolidated assets of less than $10 billion. Community Development Financial Institutions are a special class of lenders and you can find a downloadable list of certified CDFIs here. There are 1,142 around the country and the list is easy to use.

There is already speculation of a third round of CARE, so now isn’t the time to sit idle.

This article was produced in collaboration with the Boston Institute for Nonprofit Journalism as part of its Pandemic Democracy Project.

HELP DIGBOSTON WEATHER THIS STORM AND CONTINUE PROVIDING ARTICLES LIKE THIS ONE

David Rabinovitz is a cannabis business consultant in Massachusetts and involved in various cannabis ventures. He is a former Director and Treasurer of MassCann (the Massachusetts Cannabis Reform Coalition), a past Trainer for the Massachusetts Cannabis Control Commission Social Equity training program, and the original host of The Green Rush cannabis business talk show on ProCannabis Media. David speaks at various industry events on creating winning financial presentations that investors love. David’s industry insights and analysis are featured in several media outlets. Connect with David on LinkedIn at https://www.linkedin.com/in/davidrabinovitz/ or reach out to him at drabinovitz@gmail.com or DavidR@CannaVentureLabs.com